What are Fully Diluted Shares?

Fully diluted shares represent the total number of shares a company would have if all outstanding convertible securities, stock options, warrants, and similar obligations were exercised or converted into equity due to obligations triggered by a liquidity or conversion event.

A liquidity event is usually linked to a change of control in the company, such as:

More than 51% of the share capital being acquired by another company,

A merger, or

The company going public (IPO).

These shares are crucial in understanding the real ownership structure and valuation of a company.

Examples of Fully Diluted Shares

To understand how fully diluted shares impact a cap table, let’s consider a simple scenario:

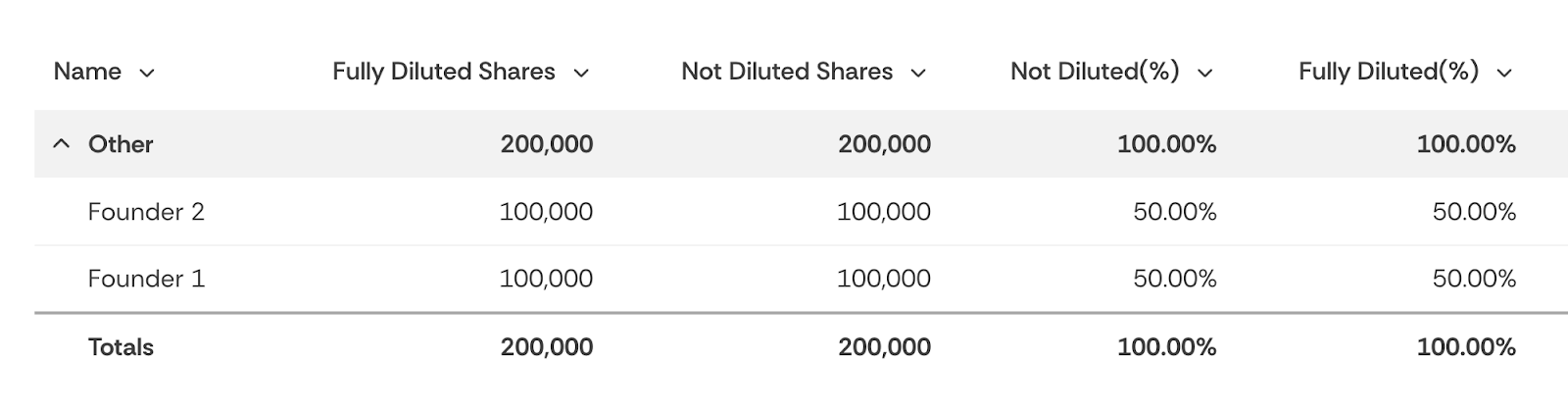

Initial Cap Table

Initially, the company has 200,000 shares issued, and there are no convertible obligations, so issued shares equal fully diluted shares.

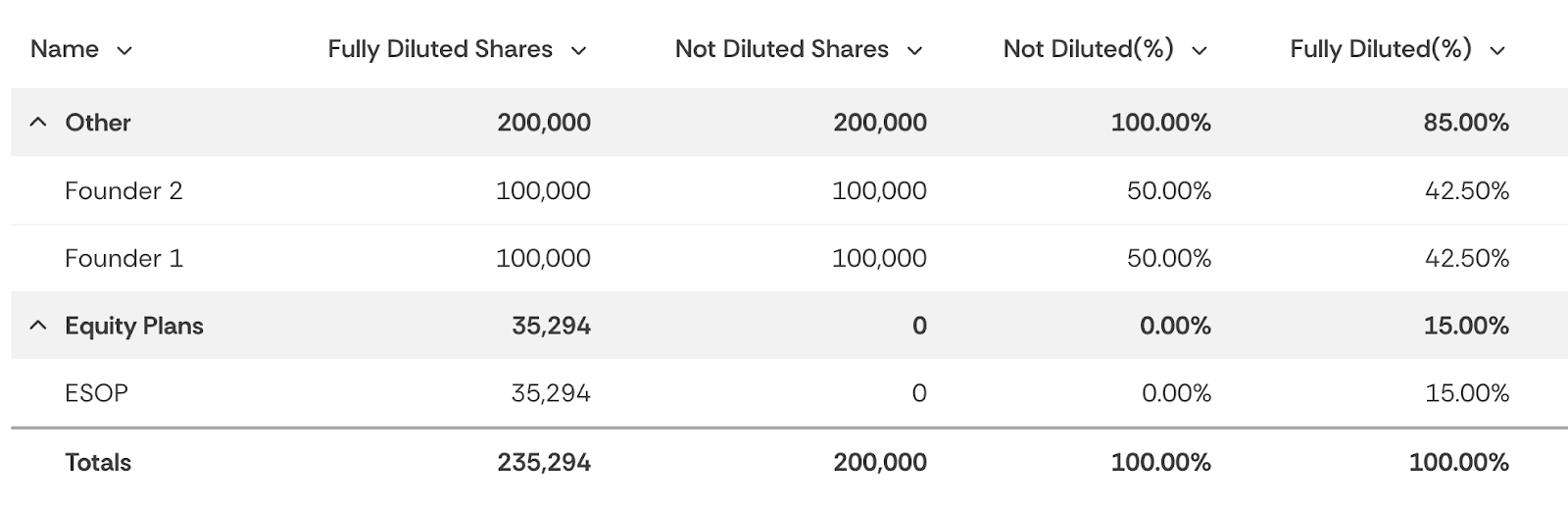

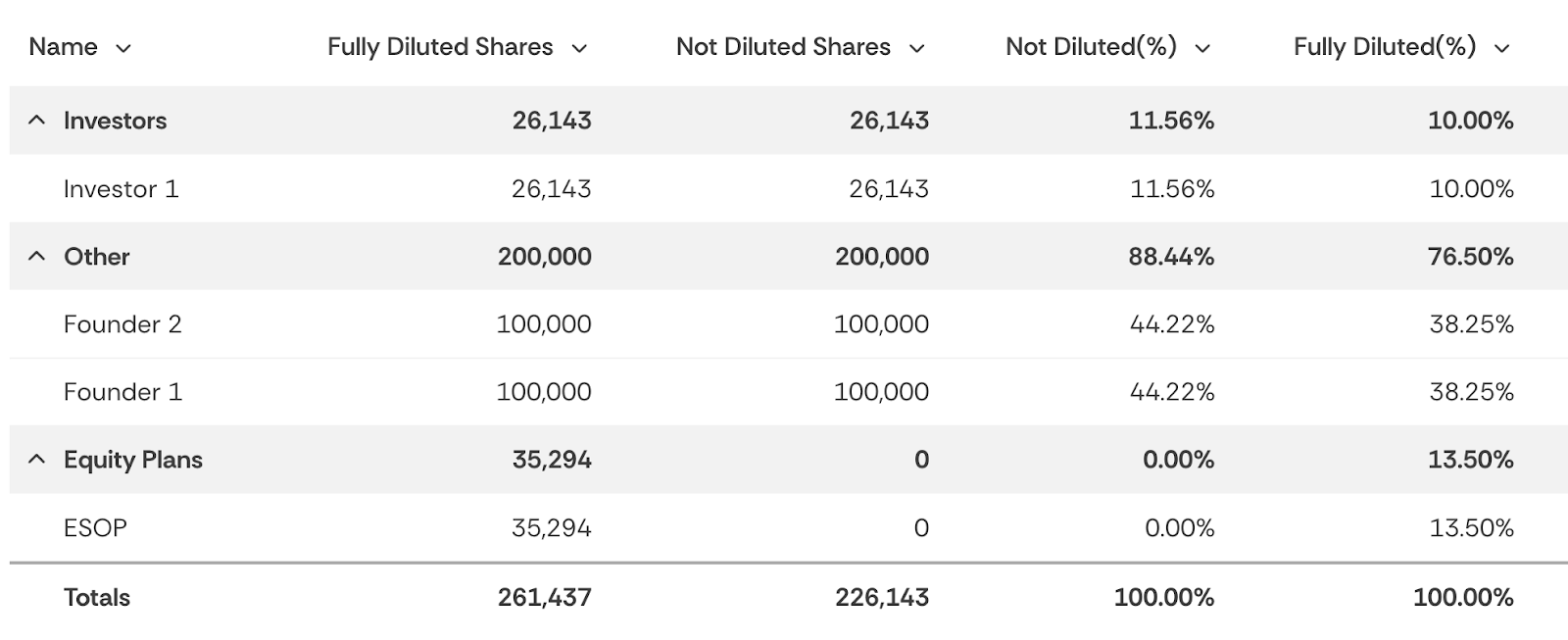

How does an ESOP impact the Cap Table?

Now, let’s introduce an Employee Stock Option Plan (ESOP) of 15% of the share capital.

This dilutes the ownership of existing shareholders. The updated cap table would look like this:

The founders retain 50% ownership of issued shares but only 42.5% of fully diluted shares.

Each Equity Plan Impacts the Cap Table Differently

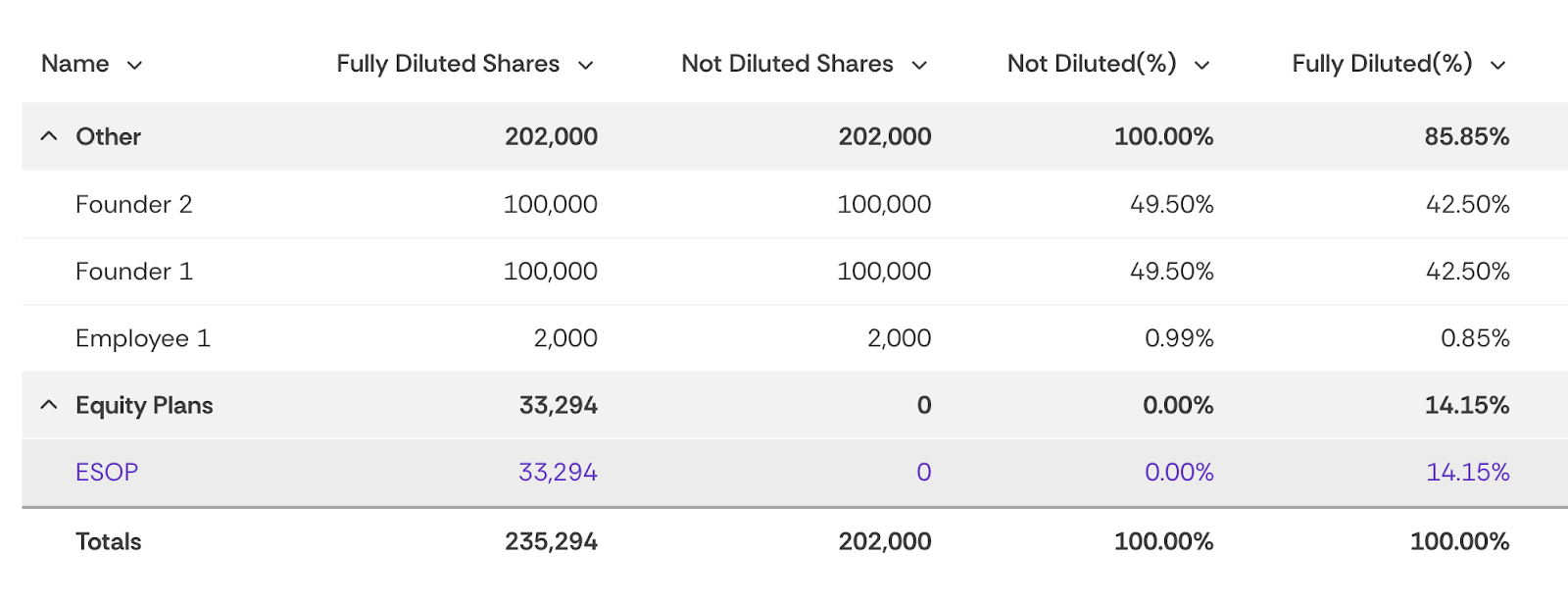

Stock options

In stock option plans, participants become part of the cap table when they vest and exercise the options granted by the company.

This impacts the governance of the company, as they acquire political rights, such as voting rights and access to company information.

For example, a cap table where the board has approved an ESOP plan might include shares already granted, vested, and exercised. All ESOP shares are typically Common shares, though companies may have different share classes to grant additional rights to specific stockholders.

Employee 1 was granted some stock options that have already vested and exercised, which are added to the Cap Table.

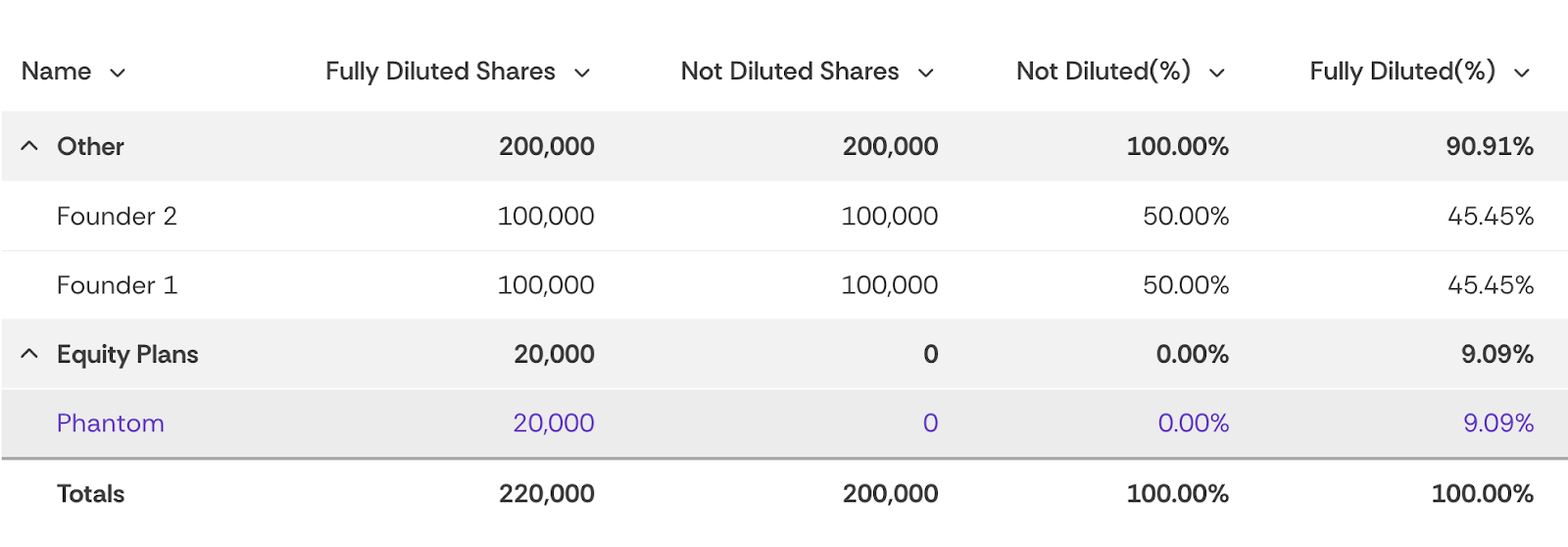

Virtual Stock Options (VSOP) and Phantom Shares

Participants in phantom share plans do not become shareholders of the company, simplifying cap table calculations.

Phantom shares appear in the non diluted cap table with 0 shares issued, but the total plan size is included in the fully diluted share count.

For example:

A company creates a phantom share plan representing 10% of the share capital (200.000*10%)

At the time of its creation, the plan represents 9.09% of the fully diluted shares, rather than the full 10%, due to its own dilution.

*In these examples, we do not take into account possible vesting acceleration clauses that some plans have. The acceleration clauses allow the plan participants to consolidate the rest of the non-vested shares when a liquidity event happens (normally by 50% or 100%). There are several modes of acceleration, but we will not go into detail in this article.

Funding Round Dilution

It is common for new stock option or phantom share plans to be introduced during funding rounds. Investors expect these plans to be implemented before they inject capital, leading to a two-step dilution process:

Dilution due to the creation of an equity plan.

Dilution from issuing shares to new investors.

For example, after adding a 15% ESOP and completing a $1M investment at a $9M fully diluted pre-money valuation, the new ownership structure might look like this:

Fully Diluted Stock Calculators

Calculating fully diluted shares can be confusing and have calculation errors in Excel.

Capboard offers several free tools for calculating and managing fully diluted shares:

Dilution calculator: Determine the number of shares needed for a new investor to achieve a specific ownership percentage.

Cap table generator: Create detailed cap tables with automated fully diluted calculations.

Cap table templates: Download ready-to-use examples for Excel or integrate with Capboard.

You can create your cap table with automated fully diluted calculation on Capboard for free.

It is simple and you will avoid calculation errors, in addition to being able to invite your shareholders.